Issuer Free Writing Prospectus dated November 25, 2022

Filed Pursuant to Rule 433 under the Securities Act of 1933

Relating to the Preliminary Prospectus dated November 23, 2022

Registration Statement No. 333-267657

CALIBERCOS INC.

This free writing prospectus relates only to the initial public offering of shares of common stock of CaliberCos Inc. (the “Company”) and should be read together with the preliminary prospectus dated November 23, 2022 (the “Preliminary Prospectus”) included in Amendment No. 2 to the Registration Statement (“Amendment No. 2”) on Form S-1 (File No. 333-267657) relating to the offering of such securities. Amendment No. 2 may be accessed through the following link: http://www.sec.gov/Archives/edgar/data/tm2230806d1_s1a.htm/000110465922121830/0001104659-22-121830-index.html

The Company has filed a registration statement (including the Preliminary Prospectus) with the Securities and Exchange Commission (the “SEC”) in connection with the offering to which this communication relates. Before you invest, you should read the Preliminary Prospectus and the other documents the Company has filed with the SEC for more complete information regarding the Company and the offering. You may obtain these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the Company, any underwriter or any dealer participating in the offering will arrange to send you a copy of the Preliminary Prospectus if you request it from: Revere Securities LLC, Attn.: Joe Giamichael, 650 Fifth Avenue, 35th Floor, New York, New York 10019, by telephone at 212-688-2350 or by email at info@reveresecurities.com.

Wealth Development for the Middle Market November 2022 ©2022 Caliber

This presentation includes statements concerning CaliberCos Inc . ’s (the “Company”) expectations, beliefs, plans, objectives, goals, strategies, assumptions of future events, future financial performance, or growth and other statements that are not historical facts . These statements are "forward - looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995 . In some cases, readers and the audience can identify these forward - looking statements through the use of words or phrases such as "estimate,“ "expect," "anticipate," "intend," "plan," "project," "believe," "forecast," "should," "could," and other similar expressions . Forward - looking statements involve risks and uncertainties that may cause actual results or outcomes to differ materially from those included in the forward - looking statements . The Company's expectations, beliefs, and projections are expressed in good faith and are believed by the Company to have a reasonable basis, but there can be no assurance that management's expectations, beliefs, or projections will be achieved or accomplished . Factors that may cause actual results to differ materially from those included in the forward - looking statements include, but are not limited to, factors affecting the Company’s ability to successfully operate and manage its business, including, among others, title disputes, weather conditions, shortages, delays, or unavailability of equipment and services, property management, brokerage, investment and fund operations, the need to obtain governmental approvals and permits, and compliance with environmental laws and regulations ; changes in costs of operations ; loss of markets ; volatility of asset prices ; imprecision of asset valuations ; environmental risks ; competition ; inability to access sufficient capital ; general economic conditions ; litigation ; changes in regulation and legislation ; economic disruptions or uninsured losses resulting from major accidents, fires, severe weather, natural disasters, terrorist activities, acts of war, cyber attacks, or pest infestation ; increasing costs of insurance, changes in coverage and the ability to obtain insurance ; and other presently unknown or unforeseen factors . Other risk factors are detailed from time to time in the Company's reports filed with the Securities and Exchange Commission . Any forward - looking statement speaks only as of the date on which such statement is made, and the Company undertakes no obligation to update the information contained in any forward - looking statements to reflect developments or circumstances occurring after the statement is made or to reflect the occurrence of unanticipated events . Past performance is not indicative of future results . There is no guarantee that any specific outcome will be achieved . Investment may be speculative and illiquid and there is a total risk of loss . There is no guarantee that any specific investment will be suitable or profitable . IThis presentation does not constitute an offering of, nor does it constitute the solicitation of an offer to buy, securities of the Company . This presentation is provided solely to introduce the Company to the recipient and to determine whether the recipient would like additional information regarding the Company and its anticipated plans . Any investment in the Company or sale of its securities will only take place pursuant to an appropriate, private placement memorandum and a detailed subscription agreement . Some of the information contained herein is confidential and proprietary to the Company and the presentation is provided to the recipient with the express understanding that without the prior written permission of the Issuer, such recipient will not distribute or release the information contained herein, make reproductions of, or use it for any purpose other than determining whether the recipient wishes additional information regarding the Company or its plans . By accepting delivery of this presentation, the recipient agrees to return same to the Company if the recipient does not wish to receive any further information regarding the Company . We have filed a registration statement (including a preliminary prospectus) with the SEC for the offering to which this communication relates . The registration statement has not yet become effective . Before you invest, you should read the preliminary prospectus in that registration statement (including the risk factors described therein) and other documents that we have filed with the SEC for more complete information . You may access these documents for free by visiting Edgar on the SEC website at httpp : // www . sec . gov CALIBERCO.COM | 8901 E MOUNTAIN VIEW RD, STE 150, SCOTTSDALE, AZ 85258 | 480.295.7600 2 T H E W E A L T H D E V E L O P M E N T C O M P A N Y

Caliber’s Vision We create strategic investments that aim to build generational wealth for our investors, community and team 3 T H E W E A L T H D E V E L O P M E N T C O M P A N Y Authenticity & Transparency | Compassion & Service | Vision & Agility Caliber’s Core Values

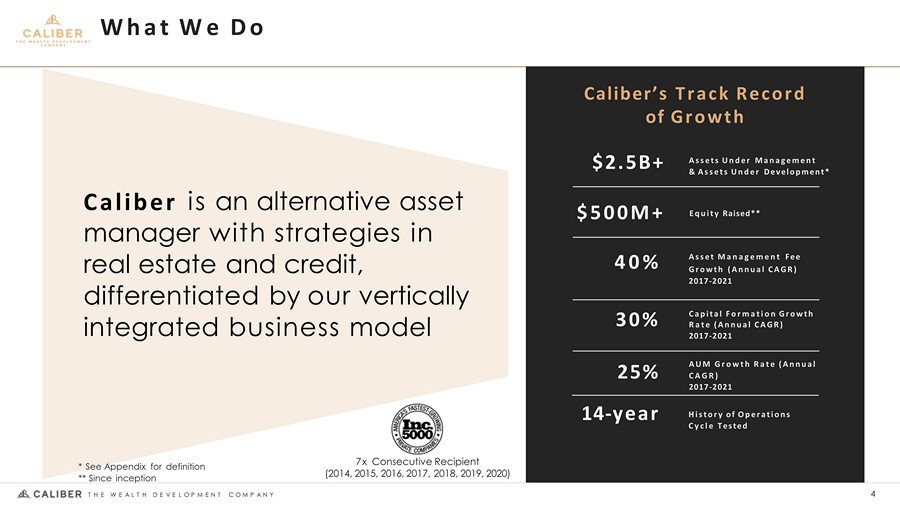

What We Do Equity Raised** $500M+ Assets Under Management & Assets Under Development* 40% Asset Management Fee Growth (Annual CAGR) 2017 - 2021 Capital Formation Growth Rate (Annual CAGR) 2017 - 2021 30% Caliber’s Track Record of Growth 25% $2.5B+ 14 - year History of Operations Cycle Tested AUM Growth Rate (Annual CAGR) 2017 - 2021 Caliber is an alternative asset manager with strategies in real estate and credit, differentiated by our vertically integrated business model 7x Consecutive Recipient (2014, 2015, 2016, 2017, 2018, 2019, 2020) 4 T H E W E A L T H D E V E L O P M E N T C O M P A N Y * See Appendix for definition ** Since inception

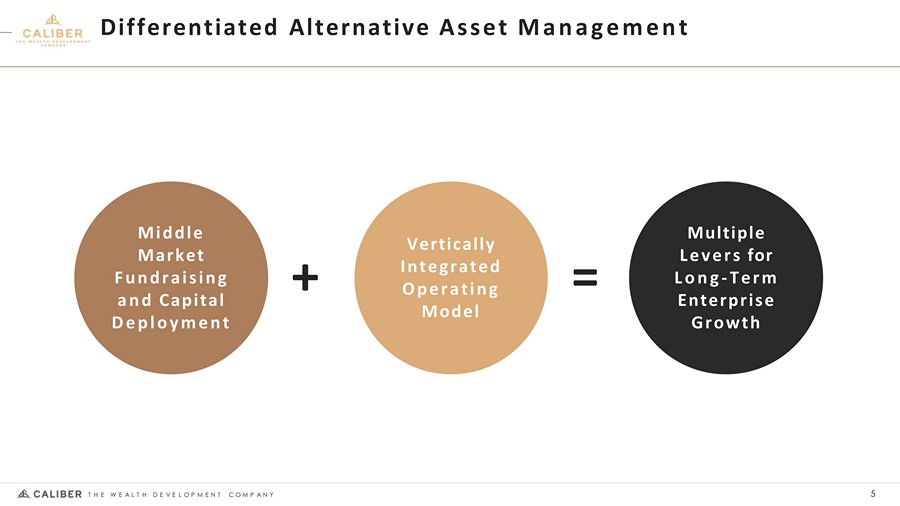

Middle Market Fundraising and Capital Deployment Vertically Integrated Operating Model Multiple Levers for Long - Term Enterprise Growth Differentiated Alternative Asset Management + 5 T H E W E A L T H D E V E L O P M E N T C O M P A N Y =

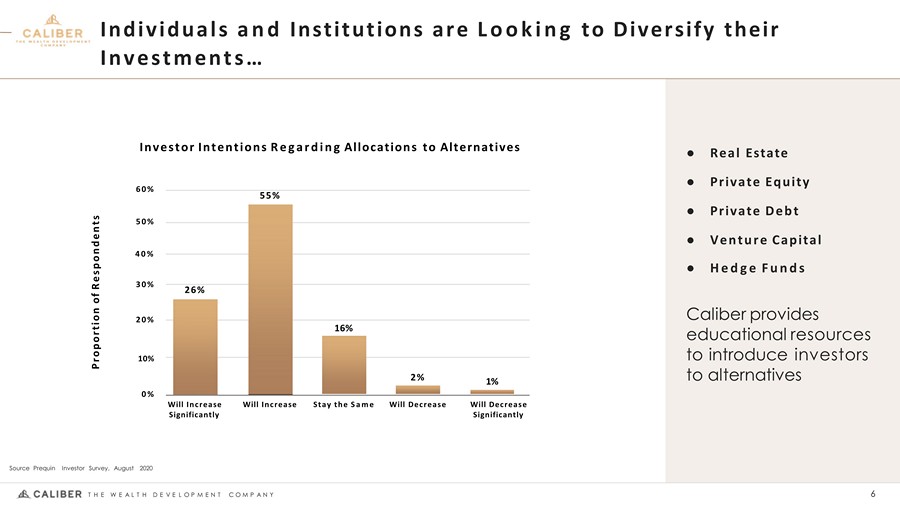

Individuals and Institutions are Looking to Diversify their Investments… Caliber provides educational resources to introduce investors to alternatives Stay the Same 2% 16% 55% 26% Will Increase Will Increase Significantly Will Decrease Significantly Will Decrease 1% 0% 10% 20% 30% Proportion of Respondents 40% 50% 60% 6 T H E W E A L T H D E V E L O P M E N T C O M P A N Y Source Prequin Investor Survey, August 2020 ● Real Estate ● Private Equity ● Private Debt ● Venture Capital ● Hedge Funds Investor Intentions Regarding Allocations to Alternatives

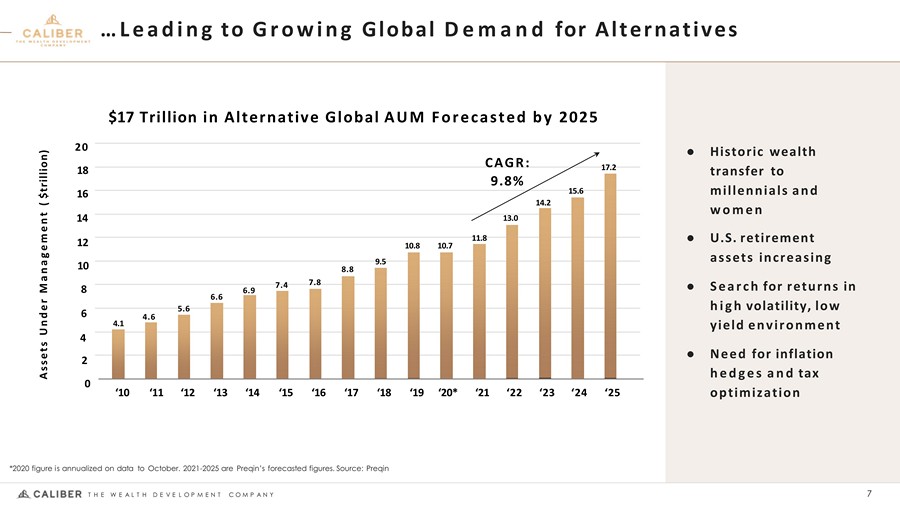

20 18 16 14 12 10 8 6 4 2 0 ‘10 ‘11 ‘12 ‘13 ‘14 ‘15 ‘16 ‘17 ‘18 ‘19 ‘20* ‘21 ‘22 ‘23 ‘24 ‘25 Assets Under Management ( $trillion) 4.1 4.6 5.6 6.6 6.9 7.4 7.8 8.8 9.5 10.8 10.7 11.8 13.0 14.2 15.6 17.2 CAGR: 9.8% …Leading to Growing Global Demand for Alternatives ● Historic wealth transfer to millennials and women ● U.S. retirement assets increasing ● Search for returns in high volatility, low yield environment ● Need for inflation hedges and tax optimization *2020 figure is annualized on data to October. 2021 - 2025 are Preqin’s forecasted figures. Source: Preqin $17 Trillion in Alternative Global AUM Forecasted by 2025 7 T H E W E A L T H D E V E L O P M E N T C O M P A N Y

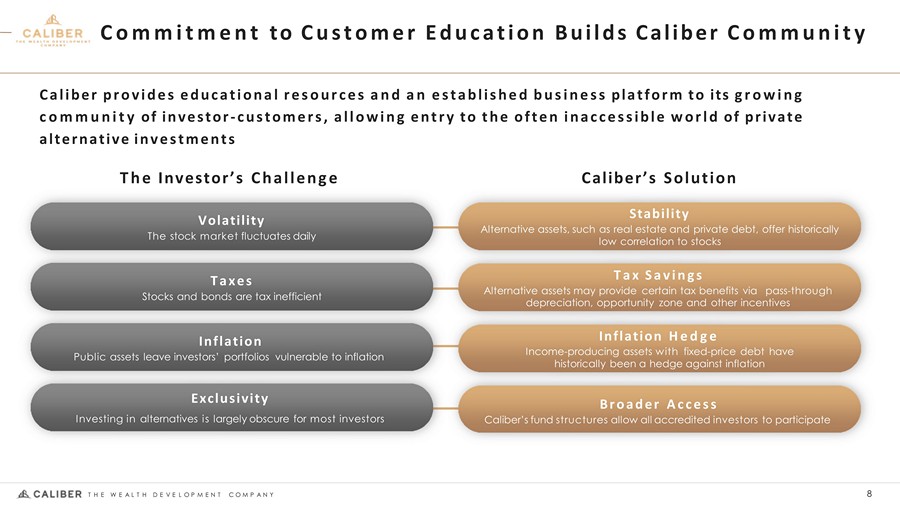

The Investor’s Challenge Commitment to Customer Education Builds Caliber Community Caliber’s Solution Stability Alternative assets, such as real estate and private debt, offer historically low correlation to stocks Volatility The stock market fluctuates daily Taxes Stocks and bonds are tax inefficient Inflation Public assets leave investors’ portfolios vulnerable to inflation Exclusivity Investing in alternatives is largely obscure for most investors Tax Savings Alternative assets may provide certain tax benefits via pass - through depreciation, opportunity zone and other incentives Inflation Hedge Income - producing assets with fixed - price debt have historically been a hedge against inflation Broader Access 8 T H E W E A L T H D E V E L O P M E N T C O M P A N Y Caliber’s fund structures allow all accredited investors to participate Caliber provides educational resources and an established business platform to its growing community of investor - customers, allowing entry to the often inaccessible world of private alternative investments

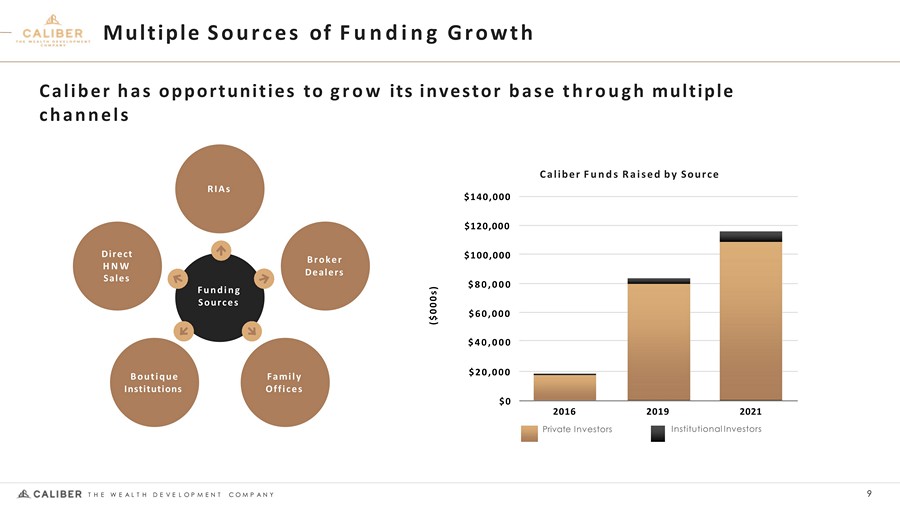

Multiple Sources of Funding Growth 2021 2019 2016 Private Investors $20,000 $60,000 $40,000 $80,000 $100,000 $120,000 $140,000 Caliber has opportunities to grow its investor base through multiple channels $0 Institutional Investors Caliber Funds Raised by Source ($000s) RIAs Broker Dealers Funding Sources Family Offices Boutique Institutions Direct HNW Sales 9 T H E W E A L T H D E V E L O P M E N T C O M P A N Y

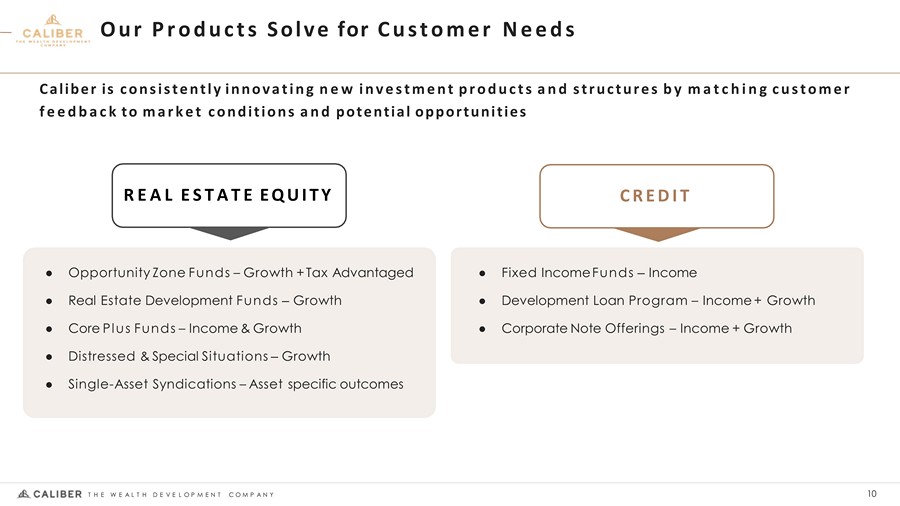

Our Products Solve for Customer Needs Caliber is consistently innovating new investment products and structures by matching customer feedback to market conditions and potential opportunities ● Opportunity Zone Funds – Growth + Tax Advantaged ● Real Estate Development Funds – Growth ● Core Plus Funds – Income & Growth ● Distressed & Special Situations – Growth ● Single - Asset Syndications – Asset specific outcomes ● Fixed Income Funds – Income ● Development Loan Program – Income + Growth ● Corporate Note Offerings – Income + Growth REAL ESTATE EQUITY CREDIT 10 T H E W E A L T H D E V E L O P M E N T C O M P A N Y

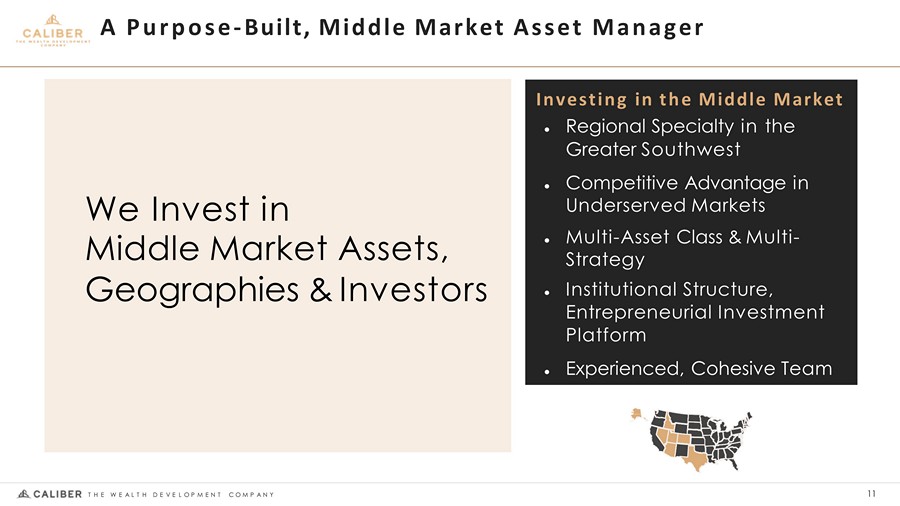

A Purpose - Built, Middle Market Asset Manager We Invest in Middle Market Assets, Geographies & Investors Investing in the Middle Market ● Regional Specialty in the Greater Southwest ● Competitive Advantage in Underserved Markets ● Multi - Asset Class & Multi - Strategy ● Institutional Structure, Entrepreneurial Investment Platform ● Experienced, Cohesive Team 11 T H E W E A L T H D E V E L O P M E N T C O M P A N Y

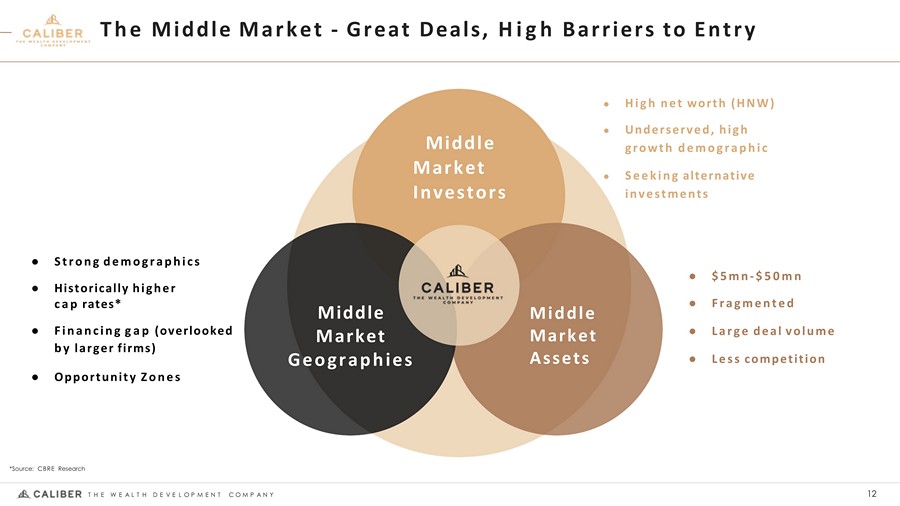

The Middle Market - Great Deals, High Barriers to Entry Middle Market Investors Middle Market Assets Middle Market Geographies ● $5mn - $50mn ● Fragmented ● Large deal volume ● Less competition ● Strong demographics ● Historically higher cap rates* ● Financing gap (overlooked by larger firms) ● Opportunity Zones ● High net worth (HNW) ● Underserved, high growth demographic ● Seeking alternative investments *Source: CBRE Research 12 T H E W E A L T H D E V E L O P M E N T C O M P A N Y

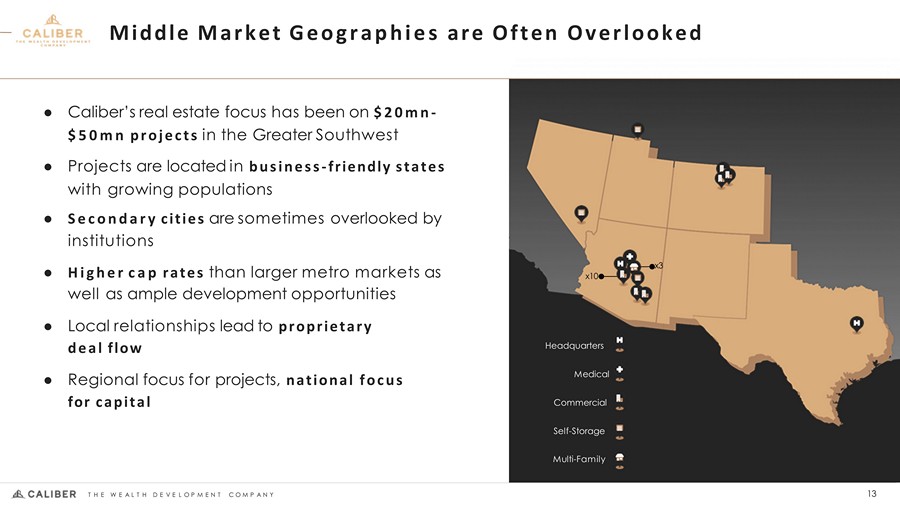

Middle Market Geographies are Often Overlooked ● Caliber’s real estate focus has been on $20mn - $50mn projects in the Greater Southwest ● Projects are located in business - friendly states with growing populations ● Secondary cities are sometimes overlooked by institutions ● Higher cap rates than larger metro markets as well as ample development opportunities ● Local relationships lead to proprietary deal flow ● Regional focus for projects, national focus for capital x3 x10 Medical Headquarters Commercial Self - Storage Multi - Family 13 T H E W E A L T H D E V E L O P M E N T C O M P A N Y

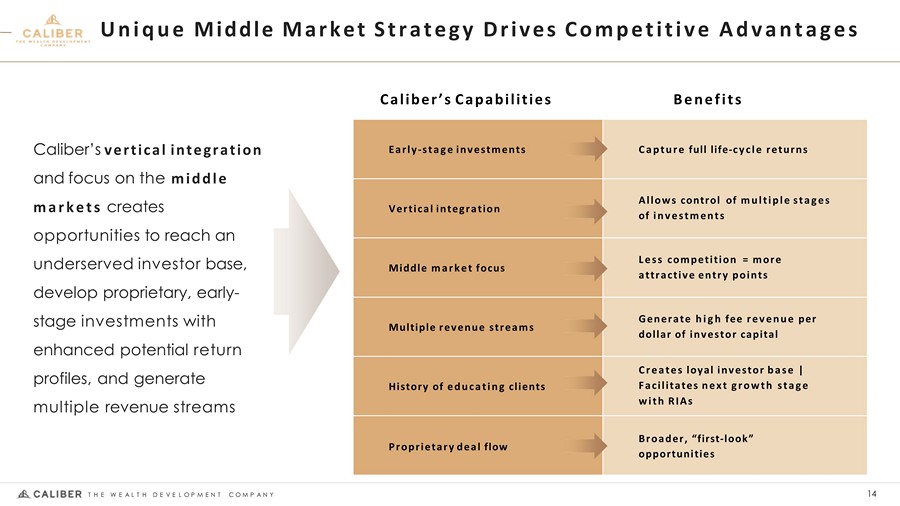

Unique Middle Market Strategy Drives Competitive Advantages Early - stage investments Capture full life - cycle returns Vertical integration Allows control of multiple stages of investments Middle market focus Less competition = more attractive entry points Multiple revenue streams Generate high fee revenue per dollar of investor capital History of educating clients Creates loyal investor base | Facilitates next growth stage with RIAs Proprietary deal flow Broader, “first - look” opportunities Caliber’s vertical integration and focus on the middle markets creates opportunities to reach an underserved investor base, develop proprietary, early - stage investments with enhanced potential return profiles, and generate multiple revenue streams Caliber’s Capabilities 14 T H E W E A L T H D E V E L O P M E N T C O M P A N Y Benefits

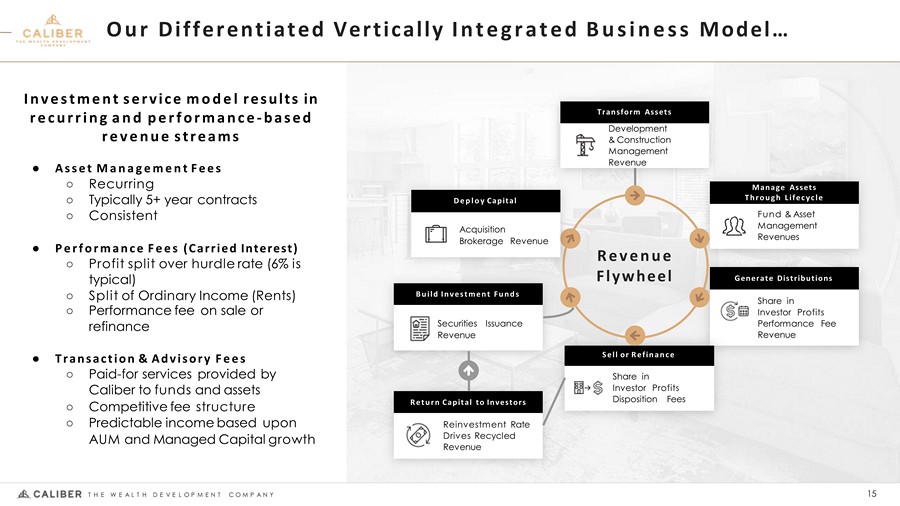

Our Differentiated Vertically Integrated Business Model… Manage Assets Through Lifecycle Fund & Asset Management Revenues Generate Distributions Share in Investor Profits Performance Fee Revenue Sell or Refinance Share in Investor Profits Disposition Fees Return Capital to Investors Reinvestment Rate Drives Recycled Revenue Build Investment Funds Securities Issuance Revenue Revenue Flywheel Transform Assets Development & Construction Management Revenue Deploy Capital Acquisition Brokerage Revenue Investment service model results in recurring and performance - based revenue streams ● Asset Management Fees ○ Recurring ○ Typically 5+ year contracts ○ Consistent ● Performance Fees (Carried Interest) ○ Profit split over hurdle rate (6% is typical) ○ Split of Ordinary Income (Rents) ○ Performance fee on sale or refinance ● Transaction & Advisory Fees ○ Paid - for services provided by Caliber to funds and assets ○ Competitive fee structure ○ Predictable income based upon AUM and Managed Capital growth 15 T H E W E A L T H D E V E L O P M E N T C O M P A N Y

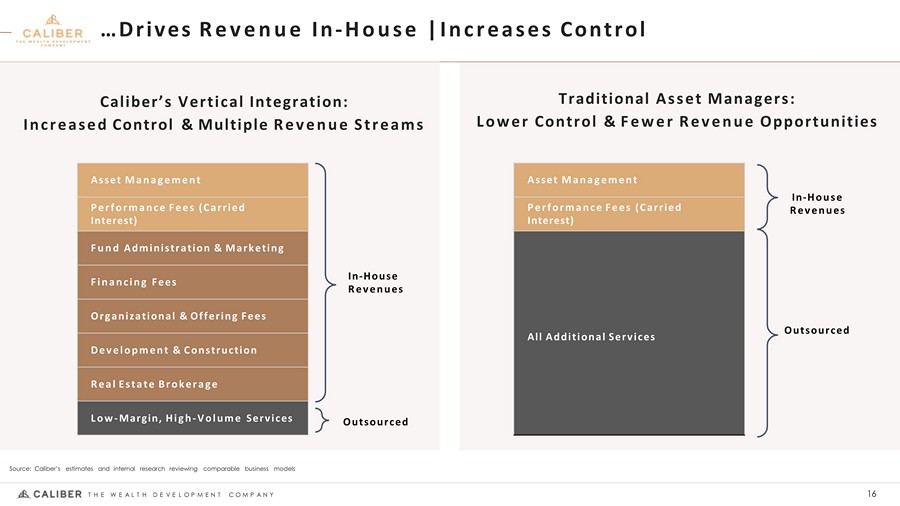

Source: Caliber’s estimates and internal research reviewing comparable business models …Drives Revenue In - House | Increases Control Caliber’s Vertical Integration: Increased Control & Multiple Revenue Streams Traditional Asset Managers: Lower Control & Fewer Revenue Opportunities Asset Management Performance Fees (Carried Interest) Fund Administration & Marketing Financing Fees Organizational & Offering Fees Development & Construction Real Estate Brokerage Low - Margin, High - Volume Services In - House Revenues 16 T H E W E A L T H D E V E L O P M E N T C O M P A N Y Outsourced Asset Management Performance Fees (Carried Interest) All Additional Services Outsourced In - House Revenues

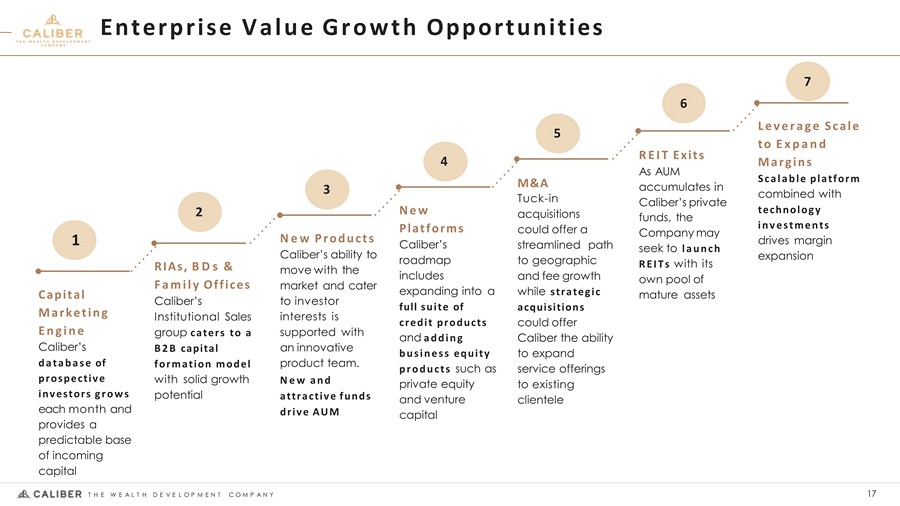

Capital Marketing Engine Caliber’s database of prospective investors grows each month and provides a predictable base of incoming capital RIAs, BDs & Family Offices Caliber’s Institutional Sales group caters to a B2B capital formation model with solid growth potential New Products Caliber’s ability to move with the market and cater to investor interests is supported with an innovative product team. New and attractive funds drive AUM New Platforms Caliber’s roadmap includes expanding into a full suite of credit products and adding business equity products such as private equity and venture capital M&A Tuck - in acquisitions could offer a streamlined path to geographic and fee growth while strategic acquisitions could offer Caliber the ability to expand service offerings to existing clientele Leverage Scale to Expand Margins Scalable platform combined with technology investments drives margin expansion REIT Exits As AUM accumulates in Caliber’s private funds, the Company may seek to launch REITs with its own pool of mature assets Enterprise Value Growth Opportunities 1 7 6 5 4 3 2 17 T H E W E A L T H D E V E L O P M E N T C O M P A N Y

Financials 18 T H E W E A L T H D E V E L O P M E N T C O M P A N Y

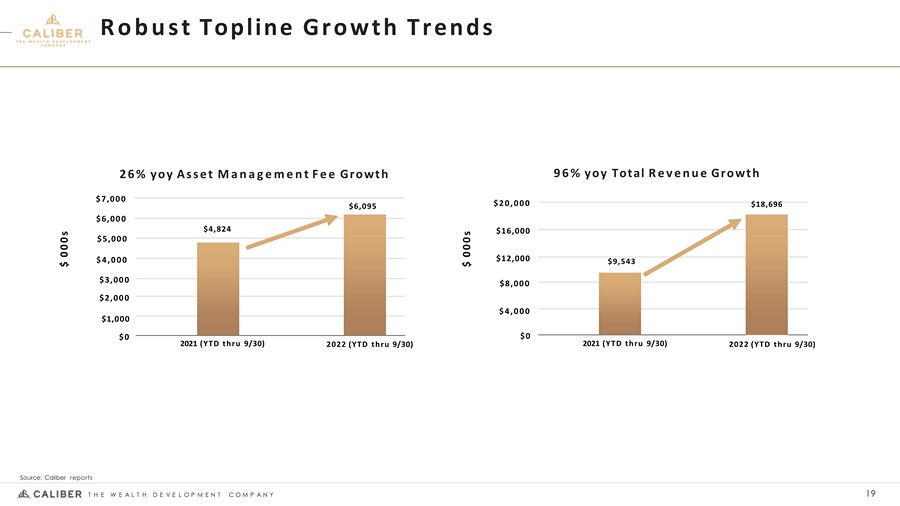

Robust Topline Growth Trends 2021 (YTD thru 9/30) $0 $4,000 $8,000 $12,000 $16,000 $20,000 96% yoy Total Revenue Growth $ 000s 2022 (YTD thru 9/30) $9,543 $18,696 2021 (YTD thru 9/30) $3,000 $2,000 $1,000 $0 $7,000 $6,000 $5,000 $4,000 26% yoy Asset Management Fee Growth $ 000s 2022 (YTD thru 9/30) $4,824 $6,095 Source: Caliber reports 19 T H E W E A L T H D E V E L O P M E N T C O M P A N Y

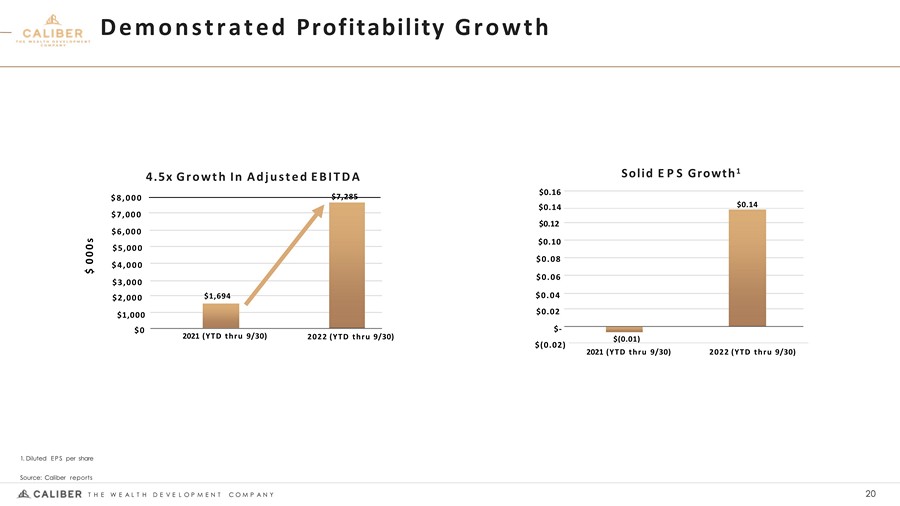

Demonstrated Profitability Growth 2021 (YTD thru 9/30) $7,000 $6,000 $5,000 $4,000 $3,000 $2,000 $1,000 $0 4.5x Growth In Adjusted EBITDA $8,000 $7,285 $ 000s 2022 (YTD thru 9/30) $1,694 1. Diluted EPS per share 2021 (YTD thru 9/30) 2022 (YTD thru 9/30) $(0.02) $ - $(0.01) $0.12 $0.10 $0.08 $0.06 $0.04 $0.02 Solid EPS Growth 1 $0.16 Source: Caliber reports 20 T H E W E A L T H D E V E L O P M E N T C O M P A N Y $0.14 $0.14

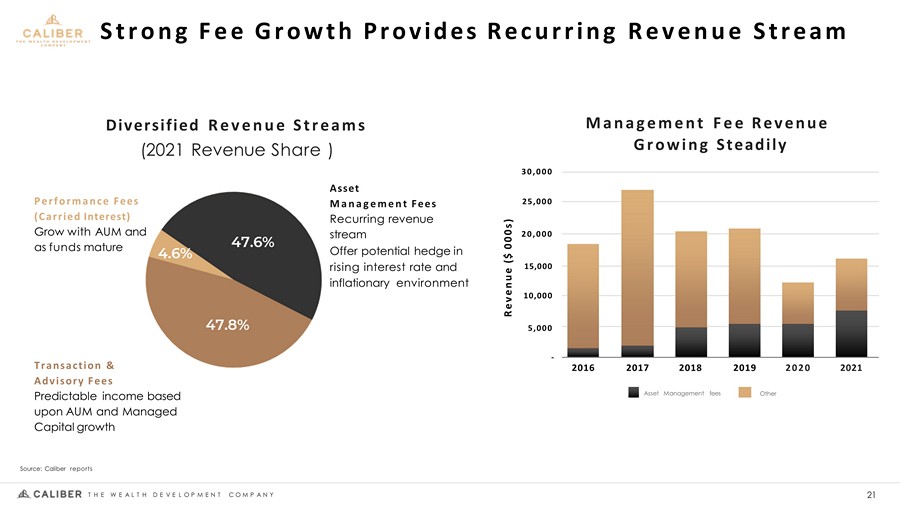

Strong Fee Growth Provides Recurring Revenue Stream Performance Fees (Carried Interest) Grow with AUM and as funds mature Transaction & Advisory Fees Predictable income based upon AUM and Managed Capital growth Asset Management Fees Recurring revenue stream Offer potential hedge in rising interest rate and inflationary environment Source: Caliber reports 2016 2020 2019 - 10,000 5,000 15,000 20,000 25,000 30,000 2017 2018 Asset Management fees Other 2021 Diversified Revenue Streams (2021 Revenue Share ) Management Fee Revenue Growing Steadily Revenue ($ 000s) 21 T H E W E A L T H D E V E L O P M E N T C O M P A N Y

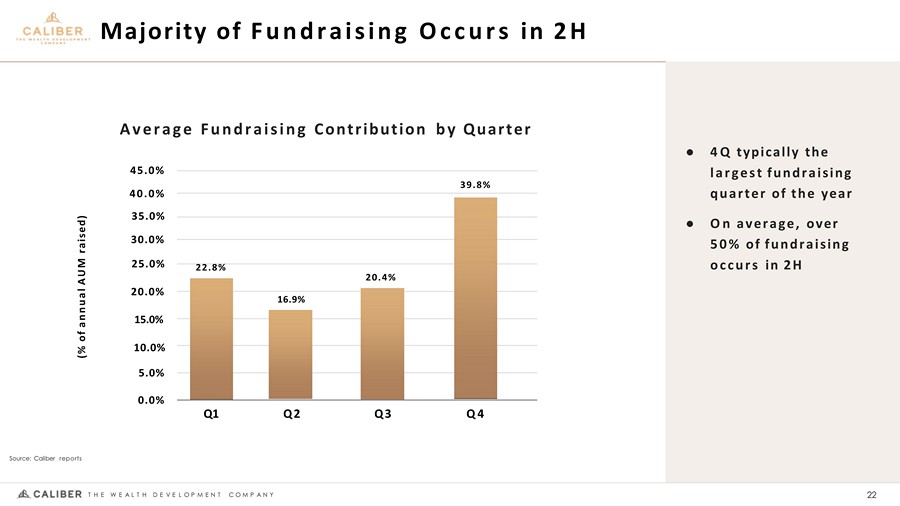

Majority of Fundraising Occurs in 2H Q2 16.9% 22.8% 22 T H E W E A L T H D E V E L O P M E N T C O M P A N Y Q1 Q3 20.4% Q4 (% of annual AUM raised) 15.0% 10.0% 5.0% 0.0% 20.0% 45.0% 40.0% 35.0% 30.0% 25.0% 39.8% Average Fundraising Contribution by Quarter ● 4Q typically the largest fundraising quarter of the year ● On average, over 50% of fundraising occurs in 2H Source: Caliber reports

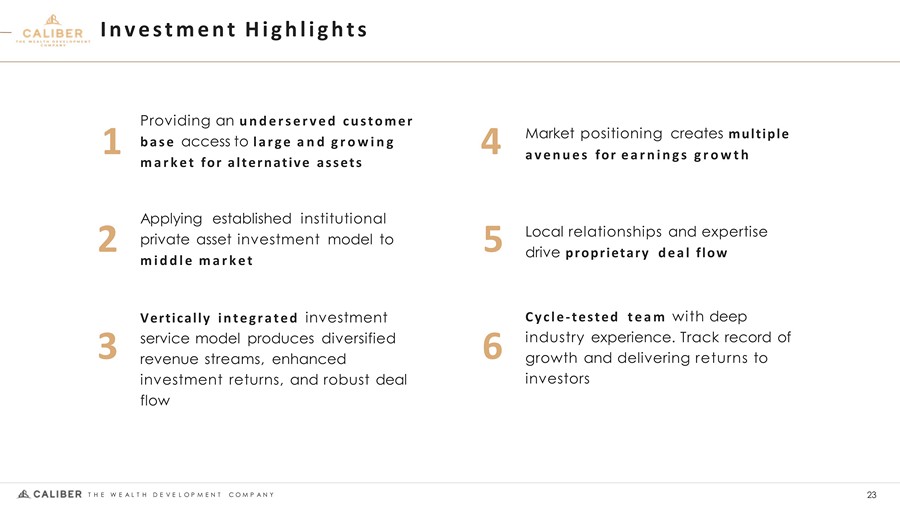

Providing an underserved customer base access to large and growing market for alternative assets Applying established institutional private asset investment model to middle market Local relationships and expertise drive proprietary deal flow Cycle - tested team with deep industry experience. Track record of growth and delivering returns to investors Vertically integrated investment service model produces diversified revenue streams, enhanced investment returns, and robust deal flow Market positioning creates multiple avenues for earnings growth Investment Highlights 2 23 T H E W E A L T H D E V E L O P M E N T C O M P A N Y 1 3 5 4 6

Appendix 24 T H E W E A L T H D E V E L O P M E N T C O M P A N Y

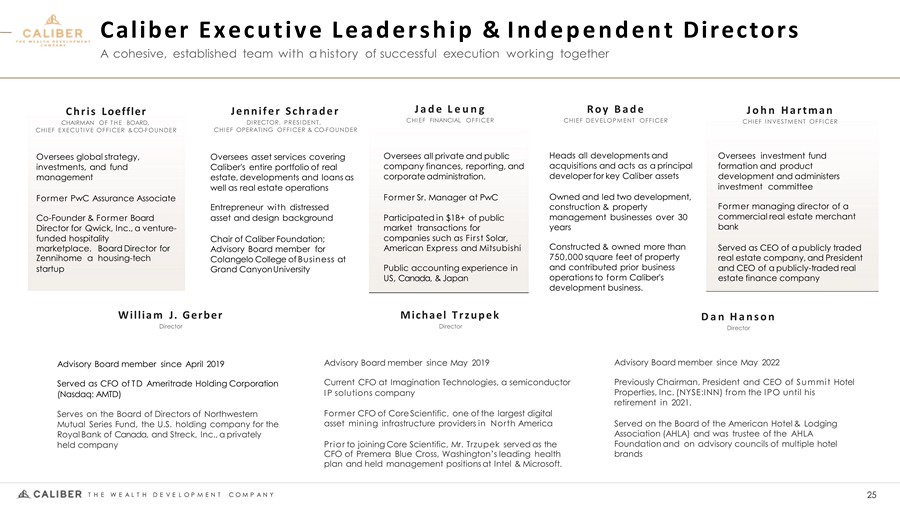

Caliber Executive Leadership & Independent Directors A cohesive, established team with a history of successful execution working together Oversees global strategy, investments, and fund management Former PwC Assurance Associate Co - Founder & Former Board Director for Qwick, Inc., a venture - funded hospitality marketplace. Board Director for Zennihome a housing - tech startup Chris Loeffler CHAIRMAN OF THE BOARD, CHIEF EXECUTIVE OFFICER & CO - FOUNDER Oversees asset services covering Caliber's entire portfolio of real estate, developments and loans as well as real estate operations Entrepreneur with distressed asset and design background Chair of Caliber Foundation; Advisory Board member for Colangelo College of Business at Grand Canyon University Jennifer Schrader DIRECTOR, PRESIDENT, CHIEF OPERATING OFFICER & CO - FOUNDER Oversees all private and public company finances, reporting, and corporate administration. Former Sr. Manager at PwC Participated in $1B+ of public market transactions for companies such as First Solar, American Express and Mitsubishi Public accounting experience in US, Canada, & Japan Jade Leung CHIEF FINANCIAL OFFICER Heads all developments and acquisitions and acts as a principal developer for key Caliber assets Owned and led two development, construction & property management businesses over 30 years Constructed & owned more than 750,000 square feet of property and contributed prior business operations to form Caliber's development business. Roy Bade CHIEF DEVELOPMENT OFFICER Oversees investment fund formation and product development and administers investment committee Former managing director of a commercial real estate merchant bank Served as CEO of a publicly traded real estate company, and President and CEO of a publicly - traded real estate finance company John Hartman CHIEF INVESTMENT OFFICER Advisory Board member since April 2019 Served as CFO of TD Ameritrade Holding Corporation (Nasdaq: AMTD) Serves on the Board of Directors of Northwestern Mutual Series Fund, the U.S. holding company for the Royal Bank of Canada, and Streck, Inc., a privately held company William J. Gerber Director Advisory Board member since May 2019 25 T H E W E A L T H D E V E L O P M E N T C O M P A N Y Current CFO at Imagination Technologies, a semiconductor IP solutions company Former CFO of Core Scientific, one of the largest digital asset mining infrastructure providers in North America Prior to joining Core Scientific, Mr. Trzupek served as the CFO of Premera Blue Cross, Washington’s leading health plan and held management positions at Intel & Microsoft. Michael Trzupek Director Advisory Board member since May 2022 Previously Chairman, President and CEO of Summit Hotel Properties, Inc. (NYSE:INN) from the IPO until his retirement in 2021. Served on the Board of the American Hotel & Lodging Association (AHLA) and was trustee of the AHLA Foundation and on advisory councils of multiple hotel brands Dan Hanson Director

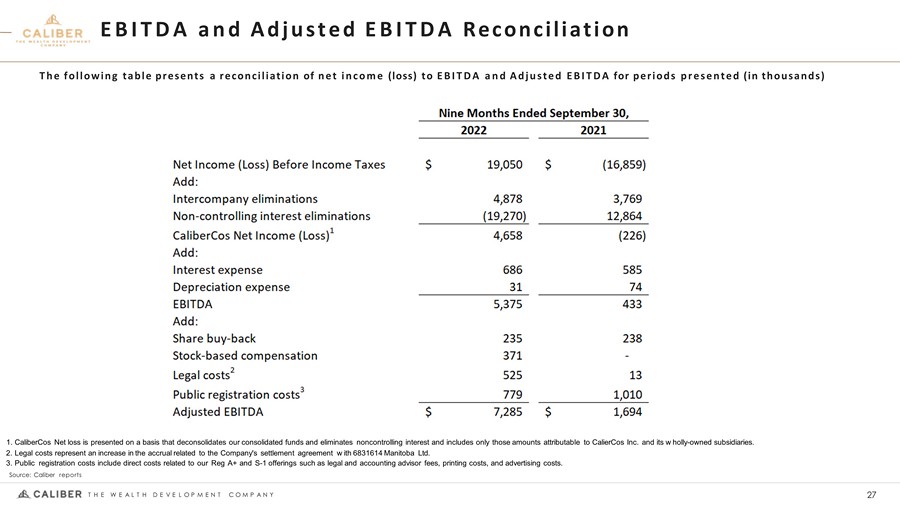

Assets Under Development. We define development, redevelopment, construction, and entitlement projects that are underway or are in the planning stages as Assets Under Development (“AUD”). This category includes projects we are planning to build on undeveloped land. If all of these projects are brought t o completion, the total cost capitalized to these projects, which represents total current estimated costs to complete the development and construction of such projects, is $2.2 billion, whic h we expect would be funded through a combination of undeployed fund cash, third - party equity, project sales, tax credit financing and similar incentives, and secured debt financing. We are under no obligation to complete these projects and may dispose of any such assets at any time. There can be no assurance that assets under development will ultimately be developed or constructed because of the nature of the cost of the approval and development process and market demand for a particular use. In addition, the mix of residential and commercial assets under development may change prior to final development. The development of these assets will require significant additional financing or other sources of funding, which may not be available. EBITDA and Adjusted EBITDA. We present EBITDA and Adjusted EBITDA , which are not recognized financial measures under U.S. GAAP, as supplemental disclosures because we regularly review these measures to evaluate our funds, measure our performance, identify trends, formulate financial projections and make strategic decisions. EBITDA represents earnings before net interest expense, income taxes, depreciation and amortization on a basis that deconsoli dates our consolidated funds (intercompany eliminations) and eliminates noncontrolling interest. Eliminating the impact of consolidated funds and noncontrolling interest provides investors a view of the performance attributable to CaliberCos Inc. and is consistent with performance models and analysis used by management. Adjusted EBITDA represents EBITDA as further adjusted to exclude stock - based compensation, transaction fees, expenses and other amounts related to the registration statement of which this prospectus forms a part, the share repurchase costs related to the Company’s Buyback Program, litigation settlements, expenses recorded to earnings relating to investment deals which were abandoned or closed, any other non - cash expenses or losses, as further adjusted for extraordinary or non - recurring items. When analyzing our operating performance, investors should use these measures in addition to, and not as an alternative for, their most directly comparable financial measure calculated and presented in accordance with U.S. GAAP. We generally use these non - U.S. GAAP financial measures to evaluate operating performance and for other discretionary purposes. We believe that these measures enhance the understanding of ongoing operations and comparability of current results to prior periods and may be useful for investors to analyze our financial performance because they eliminate the impact of selected charges that may obscure trends in the underlying performance of our business. Because not all companies use identical calculations, our presentation of EBITDA and Adjusted EBITDA may not be comparable to similarly identified measures of other companies. EBITDA and Adjusted EBITDA are not intended to be measures of free cash flow for our discretionary use because they do not consider certain cash requirements such as tax and debt service payments. These measures may also differ from the amounts calculated under similarly titled definitions in our debt instruments, which amounts are further adjusted to reflect certain other cash and non - cash charges and are used by us to determine compliance with financial covenants therein and our ability to engage in certain activities, such as incurring additional debt and making certain restricted payments. Definitions and Non - GAAP measures 26 T H E W E A L T H D E V E L O P M E N T C O M P A N Y

EBITDA and Adjusted EBITDA Reconciliation 1. CaliberCos Net loss is presented on a basis that deconsolidates our consolidated funds and eliminates noncontrolling interest and includes only those amounts attributable to CalierCos Inc. and its w holly - owned subsidiaries. 2. Legal costs represent an increase in the accrual related to the Company's settlement agreement w ith 6831614 Manitoba Ltd. 3. Public registration costs include direct costs related to our Reg A+ and S - 1 offerings such as legal and accounting advisor fees, printing costs, and advertising costs. Source: Caliber reports The following table presents a reconciliation of net income (loss) to EBITDA and Adjusted EBITDA for periods presented (in thousands) 27 T H E W E A L T H D E V E L O P M E N T C O M P A N Y